Market research firm American Lives has conducted a survey on the US wellness community market, and found a growing interest among consumers. Brooke Warrick highlights the key findings

By Brooke Warrick | Published in Spa Business 2017 issue 3

A quarter of those surveyed would like to live in a wellness community / photo: John Dolan

The study In October 2016, our market research firm, American Lives, fielded a nationwide US survey on a range of wellness issues. The study was a probability study of households with incomes over US$75,000 – the top 50 per cent in the US; the survey was completed by 1,000 respondents, aged 25 to 75 years old, which produced a demographically and statistically representative sample.

The goal was to measure the size of the market for wellness services and the likelihood that people would want these services to be available in the community where they lived.

When we divided the survey results into distinct market segments, three core market opportunities emerged. We showed that more than 75 per cent of this population wants these wellness services – and approximately 25 per cent wanted to live in such a community, while 38 per cent were inclined to visit a wellness community and would consider living there part-time.

Core market segments Three key subgroups emerged from the analysis:

Lifestyle Enthusiasts 24.8% of participants. Respondents in this segment strongly endorsed the concept of a “wellness community”, one in which they lived either full- or part-time. Members of this segment viewed their and their neighbours’ health and wellness as a core element of a family living environment.

Modest Committeds 38.8% of participants. This segment expressed an array of health and wellness values parallel to those of the Lifestyle Enthusiasts, but with a lesser level of commitment. This segment was more likely to favour health and wellness as a favourite travel investment, as opposed to a permanent lifestyle, yet at a level of interest to possibly do so through ownership of a second home. The age distribution within this segment was more tilted toward those of retirement age.

Vacation Market 12.8% of participants. Though not as dedicated as the Lifestyle Enthusiasts segment of the market, this segment still more strongly endorsed health and wellness values than the Modest Committeds, but was disinclined to express such values in a community setting. Nonetheless, they showed strong interest in owning a second home in a wellness-oriented development. This segment displayed the least disparity in age distribution within its membership, with a strong bias toward young people.

The remaining 23.6 per cent of the sample were not interested in wellness and would not be considered in the market.

In the survey, we asked a battery of questions known as the Ryff Scales of Psychological Well-Being, a widely tested and accepted series of questions that focuses on measuring multiple dimensions of psychological wellbeing. The Lifestyle Enthusiasts scored much higher on all of the wellbeing dimensions, with Modest Committeds scoring lower, and the Vacation Market somewhat lower again. This suggests that people who are objectively more psychologically healthy want to live in a community that shares and supports those values. They have a deeper understanding of what constitutes a healthy life and personal fulfillment, and they’re seeking ways to improve it; it’s at the core of what is important to them. On the other hand, the Vacation Market is interested in wellness when they have time, but it’s not a core value for them.

Key findings The demand for wellness services indicated in this study was significantly greater than expected, particularly in response to living in a wellness community. Current research by the Global Wellness Institute (GWI) signals that there is a limited supply of these communities. This is not simply an underserved market niche – it is a major market opportunity. Those Lifestyle Enthusiasts who are interested in living in a wellness community rate events and gatherings where they can engage with friends as a top feature they’d look for in a community, but they’re also interested in places for quiet, reflective, relaxing time (see fact box, p 70). Massage therapy came in second on the list of services they would be interested in, suggesting a significant role for spa operators and suppliers in the world of wellness communities.

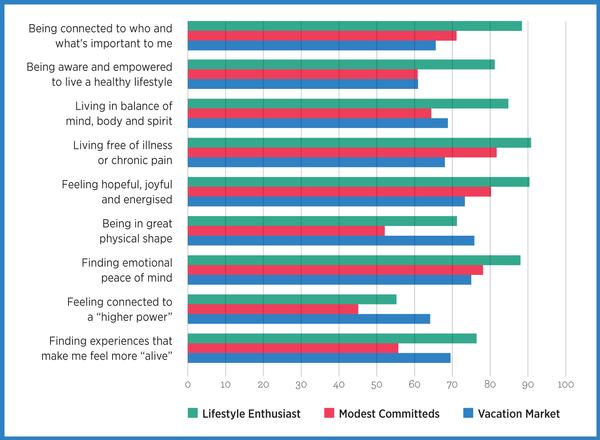

We also asked people about their attitudes and expectations of wellness services. Overall, “feeling hopeful, joyful, and energised” defines how people feel about wellness, with “living free of illness and chronic pain” a close second (see Graph 1). When correlating this data with previous trends, the desire for wellness services has grown dramatically, in large part because it’s seen as an antidote to an increasingly chaotic world. There was also further statistical evidence that people are taking more personal control of their environment, so the idea of living in a “safe haven” like a wellness community was a key driver of demand.

Read more from this issue of Attractions Management magazine

View contents of Attractions Management 2017 issue 3

Promotional feature: Elemis - Deep Benefits

With its market-leading Pro-Collagen skincare products already

a worldwide success, Elemis has further expanded its premium

anti-ageing range with a potent new seaweed-based Marine Oil

Promotional feature: RKF - a touch of luxury

As a global leader in the field of luxury

fabrics for spas and hospitality, RKF

is known for pushing the boundaries

of design and function. We find out

about the company's latest work

Top services for Lifestyle Enthusiasts For Lifestyle Enthusiasts, the following spa and wellness services were the top 10 services they were interested in 1. Events/gatherings where one can laugh and engage with friends

2. Massage therapy and other body treatments

3. Spaces for quiet, reflective time

4. Workshops on relieving stress and calming the mind

5. Access to medical professionals for specialised health programmes

6. Gourmet healthy cooking classes and nutrition classes

7. A health-oriented fine dining restaurant

8. Beauty and skincare treatments

9. A personal trainer for strength, flexibility and aerobic capacity

10. Homeopathic and alternative medicine programmes

Graph 1: Wellness attitudes by segment

Graph 1

Brooke Warrick

Brooke Warrick is president of American Lives, a market research firm that specialises in primary data collection and analyses in proprietary studies

Events to engage with friends was top of the list of services desired

Gourmet healthy cooking and nutrition classes ranked highly as a desired service

COMPANY PROFILES

Sally Corporation

Our services include: Dark ride design & build; Redevelopment of existing attractions; High-quality [more...]

Polin Waterparks

Polin was founded in Istanbul in 1976. Polin

has since grown into a leading company in

the waterpa [more...]

Painting With Light

By combining lighting, video, scenic and architectural elements, sound and special effects we tell s [more...]

Clip 'n Climb

Clip ‘n Climb currently offers facility owners and

investors more than 40 colourful and unique

Cha [more...]

An opportunity to reimagine one of the UK’s most recognisable towers has been formally

opened by Rivington Hark, as St Johns Beacon invites operators and partners to shape its

next phase. [more...]

Market research firm American Lives has conducted a survey on the US wellness community market, and found a growing interest among consumers. Brooke Warrick highlights the key findings

By Brooke Warrick | Published in Spa Business 2017 issue 3

A quarter of those surveyed would like to live in a wellness community / photo: John Dolan

The study In October 2016, our market research firm, American Lives, fielded a nationwide US survey on a range of wellness issues. The study was a probability study of households with incomes over US$75,000 – the top 50 per cent in the US; the survey was completed by 1,000 respondents, aged 25 to 75 years old, which produced a demographically and statistically representative sample.

The goal was to measure the size of the market for wellness services and the likelihood that people would want these services to be available in the community where they lived.

When we divided the survey results into distinct market segments, three core market opportunities emerged. We showed that more than 75 per cent of this population wants these wellness services – and approximately 25 per cent wanted to live in such a community, while 38 per cent were inclined to visit a wellness community and would consider living there part-time.

Core market segments Three key subgroups emerged from the analysis:

Lifestyle Enthusiasts 24.8% of participants. Respondents in this segment strongly endorsed the concept of a “wellness community”, one in which they lived either full- or part-time. Members of this segment viewed their and their neighbours’ health and wellness as a core element of a family living environment.

Modest Committeds 38.8% of participants. This segment expressed an array of health and wellness values parallel to those of the Lifestyle Enthusiasts, but with a lesser level of commitment. This segment was more likely to favour health and wellness as a favourite travel investment, as opposed to a permanent lifestyle, yet at a level of interest to possibly do so through ownership of a second home. The age distribution within this segment was more tilted toward those of retirement age.

Vacation Market 12.8% of participants. Though not as dedicated as the Lifestyle Enthusiasts segment of the market, this segment still more strongly endorsed health and wellness values than the Modest Committeds, but was disinclined to express such values in a community setting. Nonetheless, they showed strong interest in owning a second home in a wellness-oriented development. This segment displayed the least disparity in age distribution within its membership, with a strong bias toward young people.

The remaining 23.6 per cent of the sample were not interested in wellness and would not be considered in the market.

In the survey, we asked a battery of questions known as the Ryff Scales of Psychological Well-Being, a widely tested and accepted series of questions that focuses on measuring multiple dimensions of psychological wellbeing. The Lifestyle Enthusiasts scored much higher on all of the wellbeing dimensions, with Modest Committeds scoring lower, and the Vacation Market somewhat lower again. This suggests that people who are objectively more psychologically healthy want to live in a community that shares and supports those values. They have a deeper understanding of what constitutes a healthy life and personal fulfillment, and they’re seeking ways to improve it; it’s at the core of what is important to them. On the other hand, the Vacation Market is interested in wellness when they have time, but it’s not a core value for them.

Key findings The demand for wellness services indicated in this study was significantly greater than expected, particularly in response to living in a wellness community. Current research by the Global Wellness Institute (GWI) signals that there is a limited supply of these communities. This is not simply an underserved market niche – it is a major market opportunity. Those Lifestyle Enthusiasts who are interested in living in a wellness community rate events and gatherings where they can engage with friends as a top feature they’d look for in a community, but they’re also interested in places for quiet, reflective, relaxing time (see fact box, p 70). Massage therapy came in second on the list of services they would be interested in, suggesting a significant role for spa operators and suppliers in the world of wellness communities.

We also asked people about their attitudes and expectations of wellness services. Overall, “feeling hopeful, joyful, and energised” defines how people feel about wellness, with “living free of illness and chronic pain” a close second (see Graph 1). When correlating this data with previous trends, the desire for wellness services has grown dramatically, in large part because it’s seen as an antidote to an increasingly chaotic world. There was also further statistical evidence that people are taking more personal control of their environment, so the idea of living in a “safe haven” like a wellness community was a key driver of demand.

Read more from this issue of Attractions Management magazine

View contents of Attractions Management 2017 issue 3

Promotional feature: Elemis - Deep Benefits

With its market-leading Pro-Collagen skincare products already

a worldwide success, Elemis has further expanded its premium

anti-ageing range with a potent new seaweed-based Marine Oil

Promotional feature: RKF - a touch of luxury

As a global leader in the field of luxury

fabrics for spas and hospitality, RKF

is known for pushing the boundaries

of design and function. We find out

about the company's latest work

Top services for Lifestyle Enthusiasts For Lifestyle Enthusiasts, the following spa and wellness services were the top 10 services they were interested in 1. Events/gatherings where one can laugh and engage with friends

2. Massage therapy and other body treatments

3. Spaces for quiet, reflective time

4. Workshops on relieving stress and calming the mind

5. Access to medical professionals for specialised health programmes

6. Gourmet healthy cooking classes and nutrition classes

7. A health-oriented fine dining restaurant

8. Beauty and skincare treatments

9. A personal trainer for strength, flexibility and aerobic capacity

10. Homeopathic and alternative medicine programmes

Graph 1: Wellness attitudes by segment

Graph 1

Brooke Warrick

Brooke Warrick is president of American Lives, a market research firm that specialises in primary data collection and analyses in proprietary studies

Events to engage with friends was top of the list of services desired

Gourmet healthy cooking and nutrition classes ranked highly as a desired service

A new immersive attraction designed to transport visitors into the final hours of ancient Pompeii

is preparing to open near the world-famous archaeological site in southern Italy.

Experience design company, BRC Imagination Arts, has completed a transition that sees founder

Bob Rogers pass ownership of the business to four long-serving senior executives, while

remaining actively involved with the company.

Movie Park Germany has opened a new Paramount Pictures-themed attraction as part of its 30th

anniversary celebrations, using immersive storytelling and adaptive reuse to reinforce the park’s

longstanding “Hollywood in Germany” positioning.

Therme Manchester’s 28-acre development, which will include interconnected glass pavilions

that measure 65,000sq m, will be the largest bathing and wellbeing attraction in the world once

complete, according to prof David Russell, CEO of Therme UK.

Efteling has opened Hooghmoed, a new family drop tower designed to broaden the appeal of its

recently launched Sirene Island themed area and introduce younger visitors to thrill attractions.

A proposed Puy du Fou development near Bicester and Universal Destinations and Experiences’

planned resort in Bedford are emerging as part of a wider transformation of the Oxford–

Cambridge Growth Corridor into a major centre for UK leisure and tourism inv

Shedd Aquarium has opened the Immersion Theater developed in partnership with SimEx-

Iwerks, as part of a wider strategy to enhance the guest experience and create additional

revenue opportunities.

The UK government has announced a temporary reduction in VAT on visitor attractions and

children’s meals as part of a summer cost-of-living support package designed to stimulate the

visitor economy and encourage family days out.

As designer Yinka Ilori prepares for his first solo gallery show in London, he speaks exclusively

to CLADmag about his mission to spread joy, the power of play, and his bold approach to using

colour (including the colours you won’t see in his work).

The government of Thailand is exploring plans for a THB300bn (£6.3bn, US$8.3bn)

entertainment complex in the country’s Eastern Economic Corridor (EEC), with officials

proposing a large-scale theme park and sports destination as part of a broader tourism and

economic development strategy.

An opportunity to reimagine one of the UK’s most recognisable towers has been formally

opened by Rivington Hark, as St Johns Beacon invites operators and partners to shape its

next phase. [more...]