In the penultimate part of this series by industry consultant David Camp, understand how to assess profitability and predict whether a new venture will deliver adequate returns

By David Camp | Published in Attractions Management 2017 issue 3

Bellewaerde in Belgium is one of many parks operated

by Compagnie des Alpes

In this series of articles, we have discussed demand volumes, revenues and operating costs. Combining these leads to the critical assessment of profit or loss for a business, helping us answer the question – is it worth it?

While there is no standard financial reporting method for visitor attractions specifically, a common measure of the profits of a business is an assessment of the EBITDA (earnings before interest, tax, depreciation and amortisation). This effectively measures the core business operation and also allows comparison between attractions businesses.

Comparing the EBITDA to the total revenue provides a measure of the profit margin for the business. All too often, promoters of development projects over-state the potential profits, either through an over-estimation of the income or understating the operating costs, or both.

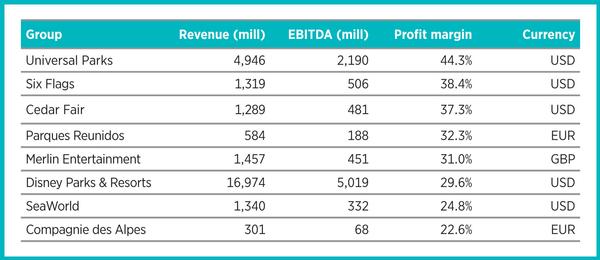

Analysing income Table 1 provides revenues and profit margins for 2016 from the annual reports for a number of attractions operating groups. The average profit margin across the sample is 32.5 per cent, although, as shown, there are some variances, with Universal Parks performing particularly well on the back of the popularity of their Harry Potter-themed attractions. The continuing negative press coverage around keeping killer whales in captivity and the Blackfish film is impacting SeaWorld’s performance, while Compagnie des Alpes continues to wrestle with operating a diverse range of medium and small attractions across Europe.

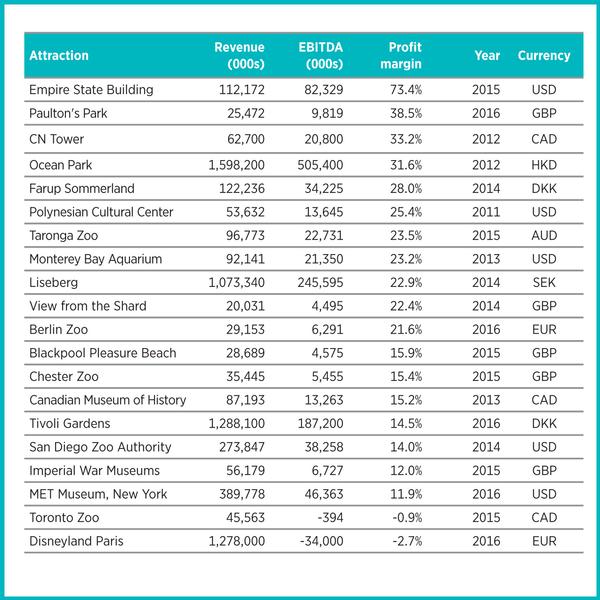

With each group operating a number of attractions, these consolidated figures mask stronger or weaker individual attraction operations. While details for individual attractions within these groups are not publicly available, there is published information available on the performance of a range of visitor attractions. We show the performance across a selection of individual attractions in Table 2.

Talking margins The list includes a number of theme parks, entertainment attractions, museums and wildlife attractions. As shown, the majority of the attractions listed achieve EBITDA margins between 10 per cent and 40 per cent, with an average of 22 per cent. These margins are generally lower than the averages achieved by the major operators, reflecting the experience of these operating groups.

While almost all of the attractions report a positive EBITDA margin, a number of them require significant financial support from grants, donations or endowments to be able to deliver these returns. This is common with many museums and wildlife attractions where visitor revenues account for less than half of the annual revenues and it is only through external funding that the attractions can continue to operate.

As shown, while attraction operations can be profitable, even for the strongest commercial operators it is difficult to exceed profit margins of more than 35 per cent. This leads to the question of what attractions are worth and how much should be invested to create new attractions?

An attraction’s value For visitor attractions, valuations are based on the earnings of the business, regardless of the amount invested. Sometimes there is an additional value associated with a building, if owned, but for most attractions there is little alternative use that the assets could be put to. Therefore, attractions are valued on a multiple of their EBITDA.

The assessment of what multiple to use depends upon a number of factors, such as the future potential of the business, whether the current EBITDA is strong or weak, the quality of the assets, how much future investment will be needed at the attractions, and the appetite of the investor for the business.

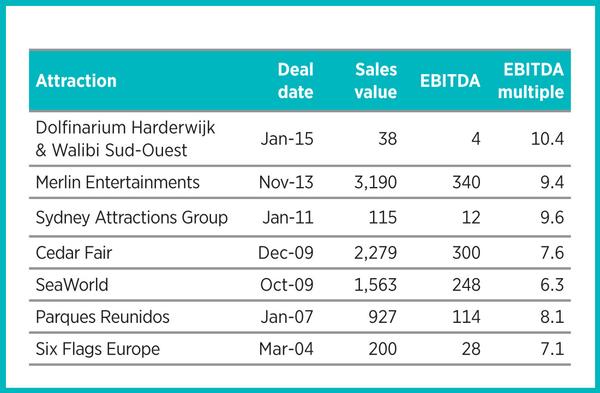

Table 3 shows examples of attraction sales and the associated EBITDA multiple. The average EBITDA multiple across the deals is just over eight, meaning that, in general, attractions are worth around eight times their annual profits. This is a useful guideline for the scale of investment that can be supported by a new attraction.

However, this presents a challenge for developers and designers of new attractions, as it is often difficult to create the scale and vision that a developer is seeking for budgets that can be supported by the business and deliver a return.

Forecasting success It is not uncommon for promoters of new projects to develop a bottom-up business plan based on a target investment level, with operating revenue and cost forecasts created to justify the scale of investment. Typically, these plans are over-optimistic, have little relationship to the size of the markets or demand levels, and do not reflect industry performance benchmarks. This may not stop them getting funded and built, but it often leads to financial problems when the operation cannot deliver on the forecasts.

Successful attractions developers and operators, such as Merlin Entertainments, understand the importance of balancing costs and values. Much of Merlin’s expansion has been through their midway attractions – Sea Life Centres, Dungeons, Madame Tussauds and Legoland Discovery Centres. These attractions are designed to a standard scale and budget, and new locations need to be able to deliver appropriate attendance levels and revenues to provide the company with a solid return on their investment. If a location cannot do this, they do not pursue the opportunity.

Success for Merlin is based on learning from past experiences and replicating proven business models. While this is not the only route to creating successful attractions, new developers would do well to take a leaf out of their book.

Read more from this issue of Attractions Management magazine

View contents of Attractions Management 2017 issue 3

Interview: Wolfgang Kiessling

We talked to Wolfgang Kiessling, who set

up a small parrot park on Tenerife in the

1970s. Today, Loro Parque and Siam Park

are some of Europe’s top attractions

Promotional feature: Sysco Productions

Sysco Productions is a world-class experience delivery

company, working for global clients in the museum and

heritage, exhibition, and sports and leisure industries

Series roadmap This eight-part series outlines the patterns and dynamics that define every attraction – from visitor behaviour and guest spending to operating costs and profitability CONTENTS 1. An overview 2. How are you perceived? 3. Benchmarking 4. Planning a new attraction 5. Driving revenues 6. Controlling costs 7. Is it worth it? 8. Benefits and impacts

Table 1 : Revenues and profit margins for operating groups in 2016

Table 2 : Revenues and profit margins for individual attractions

Table 3 : Sales of attractions and EBITDA multiple

David Camp, D&J International Consulting email: [email protected] website: www.djintcon.com

SeaWorld’s profit margin is impacted by negative attitudes to orcas in captivity

The Empire State Building’s visitor attraction achieves a profit margin of 73.4 per cent

Madame Tussauds and other Merlin midways are based on tried-and-tested models, and only sited at locations that meet the operator’s specific criteria

COMPANY PROFILES

RMA Ltd

RMA Ltd is a one-stop global company

that can design, build and produce from a

greenfield site upw [more...]

QubicaAMF UK

QubicaAMF is the largest and most

innovative bowling equipment provider with

600 employees worldwi [more...]

IDEATTACK

IDEATTACK is a full-service planning and

design company with headquarters in

Los Angeles. [more...]

DJW

David & Lynn Willrich started the Company

over thirty years ago, from the Audio Visual

Department [more...]

In the penultimate part of this series by industry consultant David Camp, understand how to assess profitability and predict whether a new venture will deliver adequate returns

By David Camp | Published in Attractions Management 2017 issue 3

Bellewaerde in Belgium is one of many parks operated

by Compagnie des Alpes

In this series of articles, we have discussed demand volumes, revenues and operating costs. Combining these leads to the critical assessment of profit or loss for a business, helping us answer the question – is it worth it?

While there is no standard financial reporting method for visitor attractions specifically, a common measure of the profits of a business is an assessment of the EBITDA (earnings before interest, tax, depreciation and amortisation). This effectively measures the core business operation and also allows comparison between attractions businesses.

Comparing the EBITDA to the total revenue provides a measure of the profit margin for the business. All too often, promoters of development projects over-state the potential profits, either through an over-estimation of the income or understating the operating costs, or both.

Analysing income Table 1 provides revenues and profit margins for 2016 from the annual reports for a number of attractions operating groups. The average profit margin across the sample is 32.5 per cent, although, as shown, there are some variances, with Universal Parks performing particularly well on the back of the popularity of their Harry Potter-themed attractions. The continuing negative press coverage around keeping killer whales in captivity and the Blackfish film is impacting SeaWorld’s performance, while Compagnie des Alpes continues to wrestle with operating a diverse range of medium and small attractions across Europe.

With each group operating a number of attractions, these consolidated figures mask stronger or weaker individual attraction operations. While details for individual attractions within these groups are not publicly available, there is published information available on the performance of a range of visitor attractions. We show the performance across a selection of individual attractions in Table 2.

Talking margins The list includes a number of theme parks, entertainment attractions, museums and wildlife attractions. As shown, the majority of the attractions listed achieve EBITDA margins between 10 per cent and 40 per cent, with an average of 22 per cent. These margins are generally lower than the averages achieved by the major operators, reflecting the experience of these operating groups.

While almost all of the attractions report a positive EBITDA margin, a number of them require significant financial support from grants, donations or endowments to be able to deliver these returns. This is common with many museums and wildlife attractions where visitor revenues account for less than half of the annual revenues and it is only through external funding that the attractions can continue to operate.

As shown, while attraction operations can be profitable, even for the strongest commercial operators it is difficult to exceed profit margins of more than 35 per cent. This leads to the question of what attractions are worth and how much should be invested to create new attractions?

An attraction’s value For visitor attractions, valuations are based on the earnings of the business, regardless of the amount invested. Sometimes there is an additional value associated with a building, if owned, but for most attractions there is little alternative use that the assets could be put to. Therefore, attractions are valued on a multiple of their EBITDA.

The assessment of what multiple to use depends upon a number of factors, such as the future potential of the business, whether the current EBITDA is strong or weak, the quality of the assets, how much future investment will be needed at the attractions, and the appetite of the investor for the business.

Table 3 shows examples of attraction sales and the associated EBITDA multiple. The average EBITDA multiple across the deals is just over eight, meaning that, in general, attractions are worth around eight times their annual profits. This is a useful guideline for the scale of investment that can be supported by a new attraction.

However, this presents a challenge for developers and designers of new attractions, as it is often difficult to create the scale and vision that a developer is seeking for budgets that can be supported by the business and deliver a return.

Forecasting success It is not uncommon for promoters of new projects to develop a bottom-up business plan based on a target investment level, with operating revenue and cost forecasts created to justify the scale of investment. Typically, these plans are over-optimistic, have little relationship to the size of the markets or demand levels, and do not reflect industry performance benchmarks. This may not stop them getting funded and built, but it often leads to financial problems when the operation cannot deliver on the forecasts.

Successful attractions developers and operators, such as Merlin Entertainments, understand the importance of balancing costs and values. Much of Merlin’s expansion has been through their midway attractions – Sea Life Centres, Dungeons, Madame Tussauds and Legoland Discovery Centres. These attractions are designed to a standard scale and budget, and new locations need to be able to deliver appropriate attendance levels and revenues to provide the company with a solid return on their investment. If a location cannot do this, they do not pursue the opportunity.

Success for Merlin is based on learning from past experiences and replicating proven business models. While this is not the only route to creating successful attractions, new developers would do well to take a leaf out of their book.

Read more from this issue of Attractions Management magazine

View contents of Attractions Management 2017 issue 3

Interview: Wolfgang Kiessling

We talked to Wolfgang Kiessling, who set

up a small parrot park on Tenerife in the

1970s. Today, Loro Parque and Siam Park

are some of Europe’s top attractions

Promotional feature: Sysco Productions

Sysco Productions is a world-class experience delivery

company, working for global clients in the museum and

heritage, exhibition, and sports and leisure industries

Series roadmap This eight-part series outlines the patterns and dynamics that define every attraction – from visitor behaviour and guest spending to operating costs and profitability CONTENTS 1. An overview 2. How are you perceived? 3. Benchmarking 4. Planning a new attraction 5. Driving revenues 6. Controlling costs 7. Is it worth it? 8. Benefits and impacts

Table 1 : Revenues and profit margins for operating groups in 2016

Table 2 : Revenues and profit margins for individual attractions

Table 3 : Sales of attractions and EBITDA multiple

David Camp, D&J International Consulting email: [email protected] website: www.djintcon.com

SeaWorld’s profit margin is impacted by negative attitudes to orcas in captivity

The Empire State Building’s visitor attraction achieves a profit margin of 73.4 per cent

Madame Tussauds and other Merlin midways are based on tried-and-tested models, and only sited at locations that meet the operator’s specific criteria

Abu Dhabi-based investment firm Mubadala Capital has made a binding, fully financed

€1 billion

offer to acquire Pierre and Vacances SA, the European holiday resort operator behind the

continental European Center Parcs business.

Disney has reaffirmed its commitment to investing US$30 billion in its US parks and cruise

business by 2033, using new America250 celebrations to underline the role its attractions play

in supporting jobs, tourism and economic growth.

Expo 2030 Riyadh is being planned as a permanent visitor destination, with organisers

confirming the six-million-square-metre site will become a Global Village after the event closes.

The owner of one of Australia's best-known waterparks has acquired a major competitor,

creating a new attractions business spanning two of the country's largest visitor destinations.

The Toverland theme park in the Netherlands has announced a €98m expansion programme

that will add a resort, new attractions and staff facilities as it pursues plans to become a multi-

day destination.

Hotel de France, located on the British Isle of Jersey, has created a wellness retreat package

that includes a hot yoga session that will take place in Jersey Zoo’s butterfly sanctuary.

A new immersive attraction designed to transport visitors into the final hours of ancient Pompeii

is preparing to open near the world-famous archaeological site in southern Italy.

Experience design company, BRC Imagination Arts, has completed a transition that sees founder

Bob Rogers pass ownership of the business to four long-serving senior executives, while

remaining actively involved with the company.

Movie Park Germany has opened a new Paramount Pictures-themed attraction as part of its 30th

anniversary celebrations, using immersive storytelling and adaptive reuse to reinforce the park’s

longstanding “Hollywood in Germany” positioning.

Therme Manchester’s 28-acre development, which will include interconnected glass pavilions

that measure 65,000sq m, will be the largest bathing and wellbeing attraction in the world once

complete, according to prof David Russell, CEO of Therme UK.

+ More news

COMPANY PROFILES

RMA Ltd RMA Ltd is a one-stop global company

that can design, build and produce from a

greenfield site upw [more...]

QubicaAMF UK QubicaAMF is the largest and most

innovative bowling equipment provider with

600 employees worldwi [more...]

IDEATTACK IDEATTACK is a full-service planning and

design company with headquarters in

Los Angeles. [more...]

DJW David & Lynn Willrich started the Company

over thirty years ago, from the Audio Visual

Department [more...]